How Inflation Impacts Your Retirement Savings (And How to Stay Ahead)

You’ve worked hard to save for retirement—don’t let inflation quietly consume your future wealth.

-

Inflation erodes the purchasing power of retirement savings—without proper planning, what seems sufficient today may fall short in the future due to rising costs.

-

Historical inflation trends in Canada reveal significant fluctuations, emphasizing the importance of accounting for potential spikes rather than relying on a fixed average rate for financial models.

-

Diversification, inflation-protected investments, and tax-advantaged accounts are key strategies to shield retirement savings from inflation and maintain financial stability.

Planning for retirement isn’t just about saving money—it’s about ensuring your savings retain their value when you need them most. Inflation can drastically affect the purchasing power of your retirement funds. This article explains how inflation works, why long-term financial projections should account for potential inflation changes, and how Canadians can safeguard their retirement savings against rising costs.

What is Inflation?

Inflation refers to a general increase in prices over time. It is typically measured using indexes like the Consumer Price Index (CPI), which tracks price changes in a fixed basket of goods. Inflation can be caused by factors such as increased demand, rising production costs, or expansion of the money supply. While moderate inflation is considered normal in a growing economy, high inflation can erode savings and make everyday expenses more costly.

Inflation Explained with Coffee

The price of a cup of coffee in Canada in the 1960s was around $0.25. Today a cup of coffee costs around $3. Fifty years from now, if inflation averages 2% per year, a cup of coffee will cost around $8.

Similarly, a $10 bill in the 1960s could buy you 40 cups of coffee, while today a $10 bill could only buy you 3. Fifty years from now it will only be able to buy you 1 cup.

This example illustrates how prices generally increase over time, and conversely, how the purchasing power of money decreases over time. That’s inflation.

How Inflation Affects Retirement Saving

Inflation is one of the biggest threats to retirement savings because it silently erodes the purchasing power of money over time. If the costs of living rise but your savings remain the same, what once seemed like a comfortable retirement fund may no longer be enough to cover your future expenses. Retirees relying on fixed pensions or annuities that aren’t inflation-adjusted may struggle to keep up with rising costs. Meanwhile, investments that don’t outpace inflation could lose value in the long run. Understanding how inflation works and planning accordingly—through diversified investments, inflation-protected assets, and strategic financial planning—can help ensure that your retirement savings maintain their worth throughout your later years.

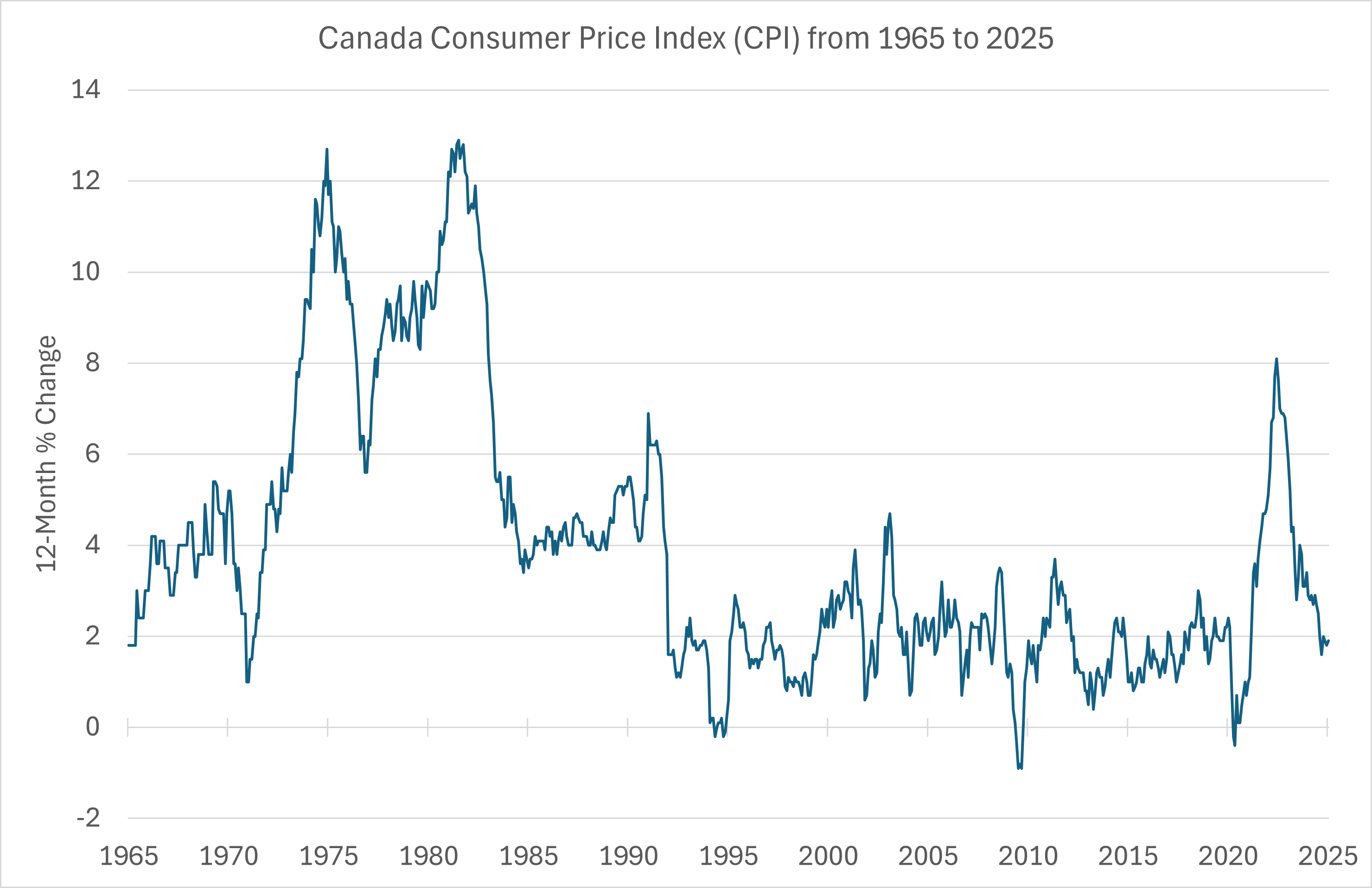

Historical Inflation Trends in Canada

Over the past 60 years, Canada has experienced varying inflation rates, with notable spikes in the early 1980s and recent fluctuations due to global economic conditions. The following plot shows inflation trends over this period, courtesy of historical CPI data from Statistic Canada’s Consumer Price Index Data Visualization Tool.

Misconceptions About Inflation

Here are a few common misconceptions about inflation:

-

Your money ‘shrinks’ over time. This is not true—$100 does not magically become $95 after a few years. Rather, $100 is simply able to buy less over that time due to the gradual increase in prices of common goods and services.

-

The government dictates the inflation rate. Many people believe that the government directly controls inflation like a switch. In reality, inflation is influenced by various economic factors, including supply and demand, global events, and central bank policies. While institutions like the Bank of Canada adjust interest rates to help manage inflation, external forces such as oil prices, trade disruptions, and consumer behavior play significant roles as well.

-

Inflation causes price increases. Inflation does not directly cause prices to rise; rather, it reflects the overall increase in prices across the economy. Prices rise due to factors like supply shortages, labor costs, and demand fluctuations, and inflation is simply the measurement of these changes over time.

Strategies to Protect Retirement Savings from Inflation

Implementing the following basic strategies help you safeguard your retirement savings from inflation and maintain financial stability despite rising costs.

-

Invest in Inflation-Protected Assets: Consider investing in assets that historically perform well during inflationary periods, such as stocks, real estate, and commodities. Additionally, Real Return Bonds (RRBs) issued by the Government of Canada adjust their value based on inflation, helping to preserve purchasing power.

-

Diversify Your Portfolio: A well-diversified investment portfolio can help mitigate inflation risks. Spreading investments across different asset classes like stocks, bonds, real estate, and international markets ensures that rising costs in one sector don’t erode your entire savings.

-

Seek Out Inflation-Indexed Retirement Income: Some pensions and annuities offer inflation-indexed payments, meaning they adjust based on the Consumer Price Index (CPI). If possible, opt for retirement income sources that provide cost-of-living adjustments to maintain purchasing power.

-

Maintain Growth-Oriented Investments: While conservative investments like fixed-income bonds may seem safe, they often struggle to keep up with inflation. Allocating a portion of your portfolio to growth-oriented investments, such as equities, can help your savings outpace inflation over time.

-

Utilize Tax-Advantaged Accounts: Maximizing contributions to Registered Retirement Savings Plans (RRSPs) and Tax-Free Savings Accounts (TFSAs) can help protect your savings from inflation while reducing tax burdens. RRSPs allow tax-deferred growth, while TFSAs provide tax-free withdrawals and tax-free growth, making them valuable tools for long-term financial security.

The Consumer Price Index (CPI)

The Consumer Price Index is a widely used measure of inflation that tracks changes in the average prices of essential goods and services over time. It reflects shifts in the cost of living, helping individuals, businesses, and policymakers understand inflation trends and their impact on financial planning.

How CPI Works

CPI is calculated by monitoring price movements in a carefully selected “basket” of goods and services that represent typical consumer spending. This includes food, housing, transportation, healthcare, and other everyday expenses. Each month, statisticians update CPI based on new price data, providing insight into economic trends.

What does CPI Track?

CPI in Canada tracks a fixed basket of goods and services that represent typical consumer spending. According to Statistics Canada, these are divided into eight major categories:

-

Food: Groceries, restaurant meals, and beverages.

-

Shelter: Rent, homeownership costs, utilities, and property taxes.

-

Household Operations, Furnishings & Equipment: Appliances, furniture, cleaning supplies, and home maintenance.

-

Clothing & Footwear: Apparel, shoes, and accessories.

-

Transportation: Vehicle purchases, fuel, public transit, and maintenance costs.

-

Health & Personal Care: Prescription drugs, dental care, and personal hygiene products.

-

Recreation, Education & Reading: Entertainment, tuition fees, books, and recreational activities.

-

Alcoholic Beverages, Tobacco & Recreational Cannabis: Alcohol, cigarettes, and legal cannabis products.

CPI is updated monthly by Statistics Canada to reflect changes in consumer habits and spending patterns. You can visit the Statistic Canada website to find out the current CPI. In April 2025, CPI was 1.7% year-over-year, meaning that the average price of the goods and services listed above increased by 1.7% since April 2024.

Limitations of CPI in Retirement Planning

Although CPI provides valuable insight into price trends, it has certain limitations. These are listed below:

-

CPI is a national average. Inflation rates fluctuate year-to-year, place to place, and category-to-category. If most of your expenses are driven by the cost of only a few expenses, and the cost of those expenses experiences significant inflation during your retirement, then you will feel as though inflation is much higher than CPI.

-

CPI does not account for changes in the value of real estate or investment assets. This is a big issue since real estate purchases typically mark the largest purchases that Canadians make during their lives. If real estate prices continue to increase at the rate they’ve followed for the past 30 years, then the cost of living in future will be significantly higher than today, but CPI won’t reflect it. Note: CPI includes shelter costs, which cover expenses related to owning and renting a home, such as mortgage interest, property taxes, rent, and homeowners’ insurance. However, it does not directly track the market price of homes. Instead, it focuses on the cost of living associated with housing. If you’re looking for a measure that tracks home prices specifically, you might want to check out the New Housing Price Index (NHPI) or other real estate market reports

-

Reflect improvements in quality. As products evolve over time their quality often improves too. This makes direct comparisons between the current and past prices of certain goods more complex than CPI might lead on.

Using CPI in Financial Models

Many financial models use an average inflation rate to estimate future costs. While this method can work for short-term projections, it carries significant risk for long-term retirement planning. Inflation rates fluctuate year-to-year, but over a short period (5-10 years), using an average inflation rate can provide reasonable estimates for budgeting. If you’re planning for retirement decades ahead, relying on a fixed average inflation rate could underestimate future costs. Canada experienced two periods of high inflation over the past fifty years:

-

During the late 1970s and early 1980s when inflation rates exceeded 10% year-over-year, far above long-term averages that are often used in financial models.

-

During the COVID-19 pandemic when global supply chains and economic uncertainty led to inflation spikes that far exceeded the 1-3% range that the Bank of Canada targets.

When it comes to long-term planning, historical examples like these highlight the importance of using either (i) more complex methods for modeling inflation, or (ii) assuming an average annual inflation rate that’s higher than the historical average CPI to ensure your model is less risky.

How Does FI Plan Account for Inflation?

FI Plan asks users to input an average annual inflation rate, which is used by the financial model that generates your retirement plan. We recommend using an average annual inflation rate of 2.5-3%. This exceeds Canada’s fifty year average of approximately 2.25%, and is therefore a is conservative assumption that you can feel good about. If your retirement plan stretches many decades into the future, we suggest using a higher inflation rate to be safer.

Note: in future FI Plan intends to let users use more complex methods of modeling inflation, based on historical inflation data, rather than just specifying an average annual inflation rate.

Conclusion

Inflation is a silent force that can erode retirement savings if not accounted for. By understanding its impact and planning accordingly, Canadians can safeguard their financial future.